The Potential for Bonding Curves and Nexus Mutual

As we saw with many projects that set arbitrary prices through overvalued ICOs, many tokens were unable to maintain a stable value due to a lack of strong economic models and tangible demand for the underlying token. With this concept in mind, we want to take this article to highlight the emergence of continuous token models, also known as bonding curves.

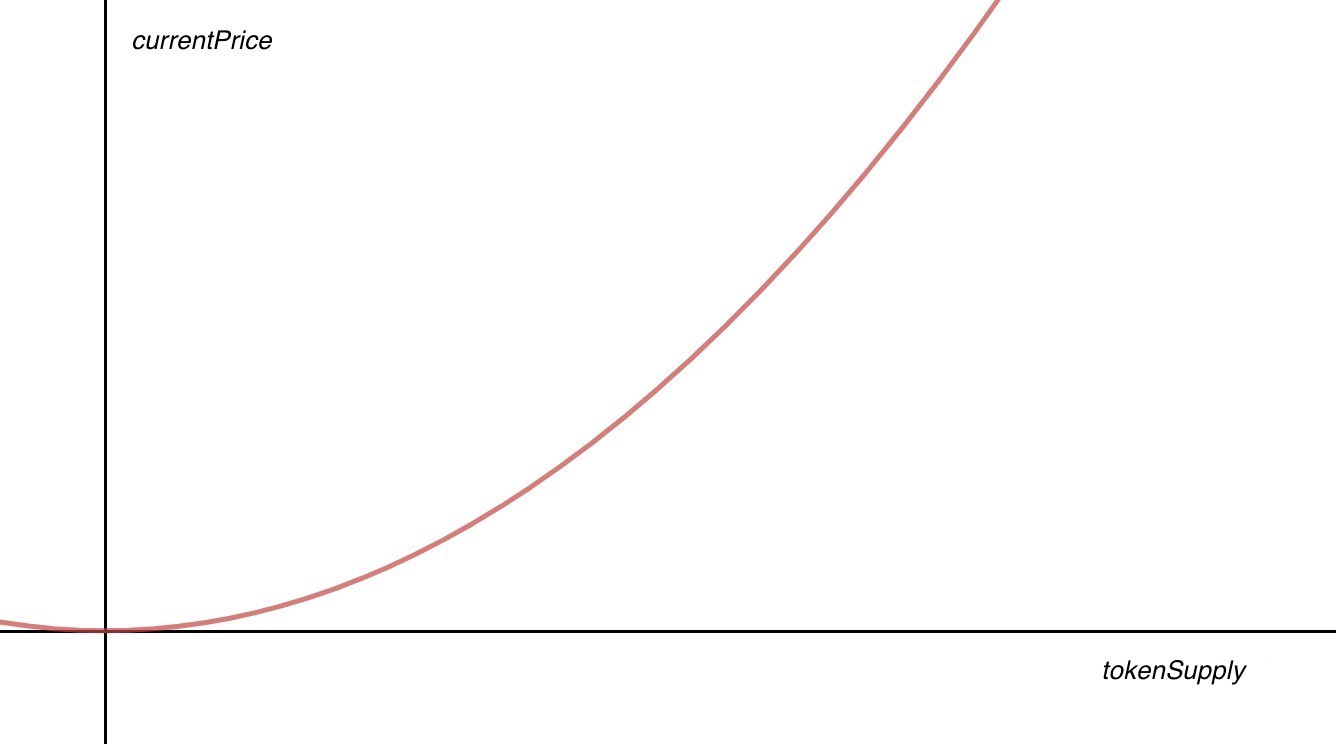

In essence, bonding curves issue new tokens each time capital (in this case ETH) is sent to the token contract. Similarly, existing tokens are burned (or destroyed) each time they are redeemed for capital (ETH) back from the token contract. In practice, bonding curves allow for the price of tokens to increase when new tokens are purchased, and decreased when existing tokens are redeemed. This is where the concept of continuous pricing comes from:

Continuous price. The price of token n is less than token n+1 and more than token n-1.

It’s important to note that the shape of a bonding curve can be altered in various ways to accomplish different economic incentives. The core tenant here is that tokens always maintain a fair value relative to the amount of collateral (ETH) stored within a contract as a reserve as any given time. For more information on bonding curves and different interpretations on how they *could* work, we recommend checking out resources here, here and here.

DeFi Insurance

It’s no surprise that most efficient markets have insurance mechanism to safeguard investors from bugs and flaws. Within the greater Ethereum ecosystem, we’ve seen more and more value being locked within smart contracts - hard written code that *could* be vulnerable to attacks.

Thanks to the proliferation of DeFi, we’re beginning to see more services utilizing smart contracts to hold and exchange value. As this aggregate value continues to grow, it’s vital for users to have access to a protocol to insure their capital.

For our more frequent readers, you may remember our post about Nexus Mutual. Over the past few weeks we’ve seen many signals that the coming months will see a plethora of upgrades that should make the protocol more accessible to the DeFi ecosystem at large - a direct catalyst for the price of the platform’s native token - NXM.

Our thesis is that as the amount of total value locked increases, the need for that value to be insured grows in parallel. With this, we can theorize that as TVL continue to increase, so will the price of NXM - thanks to the usage of a continuous token model.

What is Nexus Mutual?

Nexus Mutual is a decentralized insurance protocol built on Ethereum. While the long-term goal is to provide a broad range of insurance products, the mutual currently offers insurance on value-storing smart contracts.

The mutual uses a bonding curve to dictate token issuance, exchange trading, and price of NXM. The token represents membership rights (which is used to buy insurance covers) as well as a claim to the mutual’s capital. With that in mind, as the mutual’s capital pool increases, the value of NXM increases relative to the curve. While memberships rights is the core value proposition for NXM, the token is also used for governance over improvement proposals, claims assessment on any insurance claims, and risk assessment on smart contracts.

Graph via Nexus Mutual

If you’re looking for a full overview on Nexus Mutual, feel free to refer to our earlier Token Tuesday.

Recent Improvements and Community Updates

Earlier this month, Nexus Mutual implemented a dynamic minimum capital floor. This upgrade creates a mechanism for increasing cover capacity when the mutual has excess capital. Prior to this update, the Mutual programmatically set the max capacity per smart contract at 20% of the minimum capital requirements. This meant that no single smart contract could represent over 20% of what the Mutual could cover and is used to ensure that the mutual has a high probability of paying out all future claims.

With that, whenever there’s excess capital (in the form of MCR%) over 130%, the mutual increases its capacity by 1% per day by lowering MCR% and increasing MCR. While most members in the mutual recognized this would be a short-term detriment to price, it was vital for the prospective long-term growth of the Mutual at large.

Graph via Nexus Tracker

Since the introduction of the dynamic minimum capital floor (DMCF), the mutual has increased the mutual’s minimum capital floor by “14% over the past few weeks”. In addition, according to Nexus Tracker, the mutual has seen a 16.38% increase in active cover amounts (denominated in ETH) to over 4,710 ETH of active covers.

Graph via Nexus Tracker

Implementing the dynamic minimum capital floor was a vital iteration for the long-term growth of the mutual at large. With the DMCF now in full effect, members can have peace of mind that the mutual is more efficient in capital allocation and has a mechanism to constantly grow. As such, the growth is beginning to take notice as Nexus Mutual has allegedly been approached by multiple projects asking for large volumes to cover (around $1-2M range). However, the mutual is currently not large enough to cover these large cover amounts and therefore in need of short-term capital growth to match outstanding demand.

Via Discord, the team estimated that these large cover demands would be possible once there’s around $8-10M locked in the mutual. As such, we’re currently waiting for either (1) the mutual to accumulate more ETH or (2) the price of ETH to rise. With the capital pool only sitting at around ~10,400 ETH, we would either need 53,000 ETH locked in the mutual at an ETH price of $150 or the price of ETH to rise to $769. Either of these seem to be relatively far-fetched in the immediate short term but given that there’s over 4.5M in ETH value locked in DeFi applications, capturing a mere 1.11% of current value locked is nothing out of the ordinary for one of the only decentralized insurance products on the market.

In order for Nexus Mutual to successfully bootstrap the mutual and reach the point where it can provably insure millions in cover, the team will have to continue to iterate and lower the barriers to entry for accessing insurance benefits.

The Road Ahead

In recent developments, the core team hosted their first community call last week outlining plenty of new future upgrades that we’ll summarize below. For official call notes, visit the official Nexus Mutual Discord server

Secondary Purchases

One of the biggest needs for Nexus Mutual is the ability to reach more prospective members who would benefit from insuring their assets locked in DeFi applications. With this, the team is currently exploring implementing secondary purchases into third-party applications. Imagine lending out Dai on Compound and upon signing the transaction, there was a call-to-action asking users if they would like to purchase insurance coverage on their assets being lent out. Implementing this feature in a handful of the prominent DeFi applications would widely increase the accessibility for the mutual at large.

In order to make third-party integrations possible, the mutual will have to enable the option to operate memberships via smart contracts. By doing so, this would drastically increase integration options from third-party applications and allow aggregator-like projects to programmatically buy covers on behalf of users.

Token Economics and Incentive Reworks

As it stands today, users looking to participate in risk assessment are subject to queues for receiving rewards based on cover purchases. With that, users must lock their NXM tokens for 250 days and will only receive rewards once they’re first in the queue. Rather than relying on a queue-based rewards system, the team is exploring a new distribution model through a pooled reward system. With this system, risk assessors will be rewarded on a more consistent basis with a pro-rata rate based on the amount staked. The hope with implementing this type of rewards system is to encourage more staking activity and significantly reduce the barriers to entry when it comes to knowledge on risk assessment.

Investment Earnings

One of the more interesting things that the team is currently exploring is leveraging the existing capital pool to earn investment returns on the float. As being discussed today, this is viable in two ways: (1) integrating the Dai Savings Rate (DSR) or (2) Staking in ETH 2.0. While third-party lending applications, like Compound, will likely offer higher returns, it’s too risky for a mutual whose purpose is to insure these applications in the first place.

With $1.5M currently locked in the mutual and growing, the potential for earning investment returns on the capital pool will increase over time. By integrating the Dai Savings Rate or staking in ETH 2.0 (or both), Nexus Mutual members can receive a passive income through price appreciation of the NXM token as the capital pool increases from investment returns over time. This could be vastly important in ensuring the long-term growth of the capital pool as this mechanism would empower the dynamic minimum capital floor to increase coverage capacity over time.

Conclusion

While the growth in Nexus Mutual has been a bit slower than expected, the team is constantly iterating and will eventually come to the right formula for decentralized insurance. Moreover, as total value locked continues to rise with the proliferation of DeFi, it becomes increasingly more apparent that insurance coverage on those funds will play an important role in the maturation of the ecosystem as a whole.

With a number of new token incentives and a constant stream of governance proposals, we expect the next few months to allow Nexus to experience significant growth. Based on the underlying bonding curve implementation, we expect mutual growth to correlate to an increased price for NXM tokens.

While it hurts us to say this, it’s also likely that we will need a catalyst for the community to realize the importance of insurance. While any smart contract hack would result in a short term decrease in the price of NXM due to the mutual paying out a claim, it’s likely that a successful resolution would serve as an incredibly strong signal that the mutual’s core narrative is in fact valuable.

Until then, we recommend joining the official Discord and keeping an eye on the governance dashboard. As new proposals are made mutual members stand to earn NXM from governance participation. In summary, we’re very bullish on the future of decentralized insurance and hope that this article could shine some light on why we see Nexus Mutual being the market leader at this point in time.

*DISCLOSURE: Directors of Fitzner Blockchain do not endorse or recommend any investment action in NXM. This document should not be regarded as investment advice, offering documents, or as a recommendation regarding a course of action. Directors of Fitzner Blockchain own NXM. These views are those solely of the Directors of Fitzner Blockchain Consulting and do not represent the views of the Nexus Mutual team.