As many of us already know, Ethereum is currently the largest blockchain network in terms of functioning applications (dApps), complex logic and the sheer number of developers. Ethereum uses a turing-complete coding language, Solidity, which allows anyone to write smart contracts and decentralized applications in which arbitrary rules for ownership, transaction formats, and state transition functions can be modified by a contract’s owner(s).

For those unaware of why this concept is unique, Ethereum provided one of the first blockchain-based use cases for logic to be programmatically executed and stored on-chain via a Virtual Machine (VM) in a distributed fashion.

Whereas the Bitcoin blockchain utilizes simplistic transaction logic in the form of UTXO’s (i.e. tracking whether a transaction is spent or unspent), with Ethereum, advanced logic can be written in smart contracts and executed autonomously without the use of third parties. (i.e. upon the successful transfer of ETH, have the contract automatically perform X, Y, and Z functions).

Ethereum leverages a native currency, Ether, to execute transactions on the network. Whenever you hear the term “gas”, this simply refers to a very small amount of Ether that is consumed to reward miners for processing (or validating) your transaction. Units of ether are denoted in wei with 1,000,000,000 wei being equivalent to 1 ether.

Now that we’ve covered the basics of what Ethereum and Ether are, this article will focus more specifically on ether’s economic influences and why we believe the native currency will accrue much of the protocol’s value over the coming years.

Background

Ethereum was said to have been proposed in late 2013 by Vitalik Buterin. Shortly thereafter, the Ethereum Foundation hosted one of the very first Initial Coin Offerings (ICOs) in which reports have suggested that around $18.3M worth of ETH was sold in exchange for 31,000 BTC in July of 2014. At the time, 60M of the 72M ether was sold to investors as part of the pre-mine when the network went live in 2015. Sources have claimed that the original conversion rate was set as low as $0.10/ETH.

In the following year, a security malfunction written in the DAO’s smart contracts allowed in hackers to steal over $50M worth of ETH during a poster child offering in late 2016. This resulted in the creation of a new primary Ethereum blockchain (the one we all know today) in which the hack was reversed alongside Ethereum Classic, in which the hack was never reversed.

The next year, ETH saw the most price action in its short history during the ICO craze of 2017, in which any individual could easily create their own Ethereum-based currency in the form of ERC tokens.

To quickly summarize why ether captured so much of value, ETH is necessary to create, transact and fundraise any ERC token. As such, ether saw a massive price spike in late 2017-early 2018 as speculative investors and opportunistic entrepreneurs looked to capitalize on Initial Coin Offerings (ICOs). Eager founders flooded into the market by selling “utility tokens” that did not inherently require any KYC or were not tied to any offering of equity.

As it relates to the digital asset market today, ETH continues to be the second largest asset behind Bitcoin (BTC). During the most recent “crypto winter”, ETH has seen a significant decline from its peak (over 85% of the time of writing) and is currently exploring a new phase of price discovery as the network looks to transition to a new consensus mechanism via ETH 2.0 or Serenity (described below).

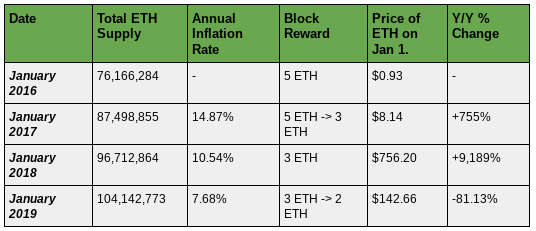

Issuance Schedule

Unlike Bitcoin’s predetermined schedule to reduce block rewards in half every 210,000 blocks, Ethereum has dynamically reduced block rewards through a series of hard forks. Over the past few years, we have seen a few forks including but not limited to the Byzantium fork in October of 2017, reducing block rewards from 5 ETH to 3 ETH (-40% change), and the most recent Constinople fork in February of 2019, reducing block rewards from 3 ETH to 2 ETH (-33.33% change).

Ethereum’s issuance rate is currently the lowest it’s ever been, and it will continue to diminish following a full transition to ETH 2.0. The network’s current issuance rate is set at approximately 4.5% per year. In comparison, Bitcoin’s current issuance rate is approximately 3.75%, where it is set to halve to 1.875% in about a year from now. With that in mind, here’s a look at how Ethereum’s the issuance schedule has played out since 2016:

As you’ll read in the next section, Ethereum’s issuance rate in 2020 and 2021 is expected to diminish to even lower rates.

ETH 2.0 (Proof of Stake)

In the past year, we’ve seen a tremendous amount of progress towards Ethereum 2.0. If you’re unfamiliar with Ethereum 2.0 (also known as Serenity or Eth2.0), it’s a series of upgrades and improvements to the network in an attempt to achieve a fully scalable and decentralized smart contract platform. These upgrades largely include two main components: (1) sharding and (2) proof of stake.

Sharding

As a very high-level overview, sharding splits a blockchain network into smaller pieces, called shards. Shards represent a chain in the network where each shard contains a set of validators. With sharding, validators are now only required to process transactions in their shard, no longer requiring every transaction to be processed and verified by every node. This shift in architectural design drastically improves the transaction throughput for Ethereum.

Proof of Stake (PoS)

Similar to how Bitcoin leverages computing power to secure the network, Ethereum 2.0 is aiming to secure the network by leveraging capital. Users (known as validators) will lock up capital, in the form of ETH, to validate transactions in return for block rewards and transaction fees.

Etherereum 2.0 is expected to roll-out gradually over the course of the next few years in a series of phases. The main phases include phases 0 - 2 where different components of sharding and PoS will be tested and implemented over time. In short, each phase can be broken down like this:

Phase 0, Beacon Chain: Initial PoS and foundational features for sharding. Validators will be able to earn rewards, however, no real transactions will be executed on this chain.

Phase 1, Basic Sharding: Network will be partitioned into shards and some transactions may process but there will be no state execution (smart contracts).

Phase 2, Sharding with EVM/EWASM: This phase introduces account balances, smart contract execution, and other abstractions into the network.

Staking Contributing to Scarcity and Security

With Ethereum 2.0 comes drastically lower issuance rates. Depending on the amount of ETH locked, the network will likely see an annual issuance rate of less than 1%. This is important to note as ETH will likely see a lower issuance rate than Bitcoin, even after the third halving in May 2020. The table below outlines the max issuance rate based on the amount of ETH locked for validating.

Table via Ethhub.io

With this, Ethereum 2.0 offers a highly scalable smart contract platform with a native asset that has a higher stock-to-flow ratio than Bitcoin, gold and obviously fiat currencies, making it highly enticing to prospective crypto investors.

ETH is Money

Proof-of-stake also allows ETH to function as money. Similar to how the incumbent financial system relies on the bond market as the foundation for yield rates, PoS creates a nearly identical system where ETH acts as the backbone for a decentralized, permissionless financial system.

As a comparison, an investor buying a bond gives the government capital to spend or lend out in return for coupon payments over a specified period of time. With PoS, an investor gives the network capital to validate transactions in return for coupon payments (in the form of issuance rewards and transaction fees) over any period of time.

Burning Mechanisms

As we migrate towards the envisioned Serenity specs, we will begin to see the inclusion of a number of new burning mechanism(s) including:

Validators Inactivity: Validators who are inactive or offline will be subject to penalties in which the system automatically withdraws the staked ETH and burns it. However, Vitalik Buterin stated in a Reddit thread that chances of inactive nodes are fairly low but, “every 1% of validators offline cuts total issuance by around 3%”.

EIP 1559:This proposal suggests burning a small percentage of transaction fees to mitigate economic inefficiencies associated with miners having the ability to choose the highest-paying transactions. Ultimately, this plays a more important role as validators begin to rely on transaction fees rather than block rewards as the driving incentive.

DeFi

For those of you who have been keeping tabs on the recent Decentralized Finance (DeFi) movement, it should come as no surprise that the large majority of projects are choosing to build on Ethereum. With this in mind, it’s important to look at DeFi as a catalyst for ETH price appreciation in the coming years and the next iteration of use cases beyond Initial Coin Offerings (ICOs).

For the vast majority of DeFi applications, ETH is locked in some way shape or form, effectively removing it from the circulating supply. As it stands today, the largest DeFi application, MakerDAO, has over 1.5M ETH (or 1.39% of the total supply) held in escrow via smart contracts to facilitate the creation of decentralized collateralized debt positions (or CDPs). Furthermore, DeFi has aggregated nearly $500M locked value via the ecosystem at large.

In the coming years, we expect DeFi to continue to grow, thus insinuating that more ETH will continue to be locked within the ecosystem as a whole.

ETH Scarcity

When combining the concepts of a diminishing issuance rate, proof of stake based consensus and a growing DeFi ecosystem, the argument for ETH value appreciation becomes quite clear. Whereas in 2017-2018 growth was driven by pure speculation of useless utility tokens, we are beginning to see more and more use-cases focusing on ETH as a base currency rather than a native ERC20 token. Furthermore, with more ERC tokens being created in the form of security tokens and stablecoins, it’s safe to assume that demand for ETH to process transactions will continue to rise in the coming years.

“Ethereum is the IBM of the smart contract blockchains: it may not be the “best” technology, but it works well enough and has amassed a distribution advantage that will be hard to overcome by its competitors.”

Concerns

While we’ve clearly taken a very positive stance on ETH in this piece, we’d like to point out that all of these assumptions rest on a successful transition to Proof of Stake via Serenity. As it stands today, Ethereum is currently only capable of processing an average of 25 transactions per second (tps), a laughable amount compared to someone like VISA who processes an average of 2000 tps.

While throughput is said to drastically increase upon the transition to ETH 2.0, it’s worth noting that the current Ethereum network recently reached 95% network capacity, resulting in high transaction fees and slow processing times. As such, without increased throughput and network capacity, growth is currently capped.

Furthermore, the community is currently divided (yet again) on the topic of ProgPoW, a proposed update to Ethereum’s consensus that would make mining less advantageous to ASIC-machines (in turn giving smaller players a higher chance at receiving block rewards). While decentralization does have its advantages, the lack of a centralized decision-making board has made upgrades and network improvements result in clear delays on large issues in the past.

Finally, compared to Bitcoin’s programmatic issuance schedule, relying on variable staking participation and case-by-case hard forks to drive scarcity through a diminishing issuance rate does create a degree of uncertainty among investors.

Conclusion

In better news, just this past week we saw the majority of ETH 2.0 clients communicating on test net, signaling that development progress is not only continuing but also reaching critical milestones.

With Ethereum’s largest annual conference, DevCon, quickly approaching, it’s no surprise that ETH has started to see some revived spirit in recent weeks. Seeing as it’s been over a year since the ICO craze officially ended, it’s safe to assume that the times of unstable projects selling their fundraised ETH on the open market has since passed. As such, we believe that in tandem with the Bitcoin halving of 2020, ETH should see strong price movement leading into the coming summer.

Written By: Cooper Turley & Lucas Campbell