Eliminating Impermanent Loss

Exploring potential designs for mitigating one of the biggest detriments to Uniswap

Hey everyone, welcome back to another week of Token Tuesdays!

Impermanent loss is one of the biggest detriments to Uniswap.

In times of high volatility, the associated losses can be a huge deterrent for liquidity providers at large. Over time it will be extremely important for the industry to explore novel mechanisms for mitigating these losses.

Ultimately if done correctly, eliminating impermanent loss will allow Uniswap to fully proliferate into an unstoppable liquidity protocol for global finance.

We explore the potential ways to mitigate these losses in this week’s release while taking a dive into the power of liquidity incentives.

Hope you enjoy it!

-Lucas and Cooper

Introduction

A few weeks back, we touched on how Uniswap (and DEXs at large) offer a new paradigm for liquidity.

With Uniswap, anyone in the world can supply capital and earn a return from exchange fees. The creation of a globally accessible liquidity protocol is likely one of the most important developments for the proliferation of DeFi in recent years. Now, any DeFi protocol can leverage Uniswap’s permissionless automated token exchange to provide liquidity for their application or product.

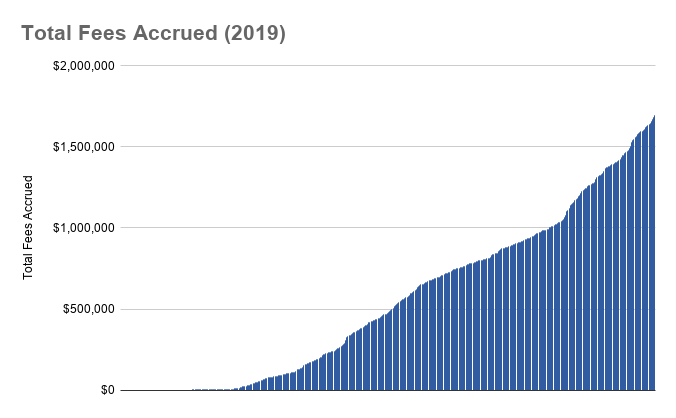

Since its inception back in November 2018, Uniswap has grown to become quite a success within the ecosystem, reaching $50M in total value locked and distributing over $1.6M to liquidity providers.

Graph via DeFi Rate Uniswap to $1B?

However, there is one looming threat to its success - impermanent loss.

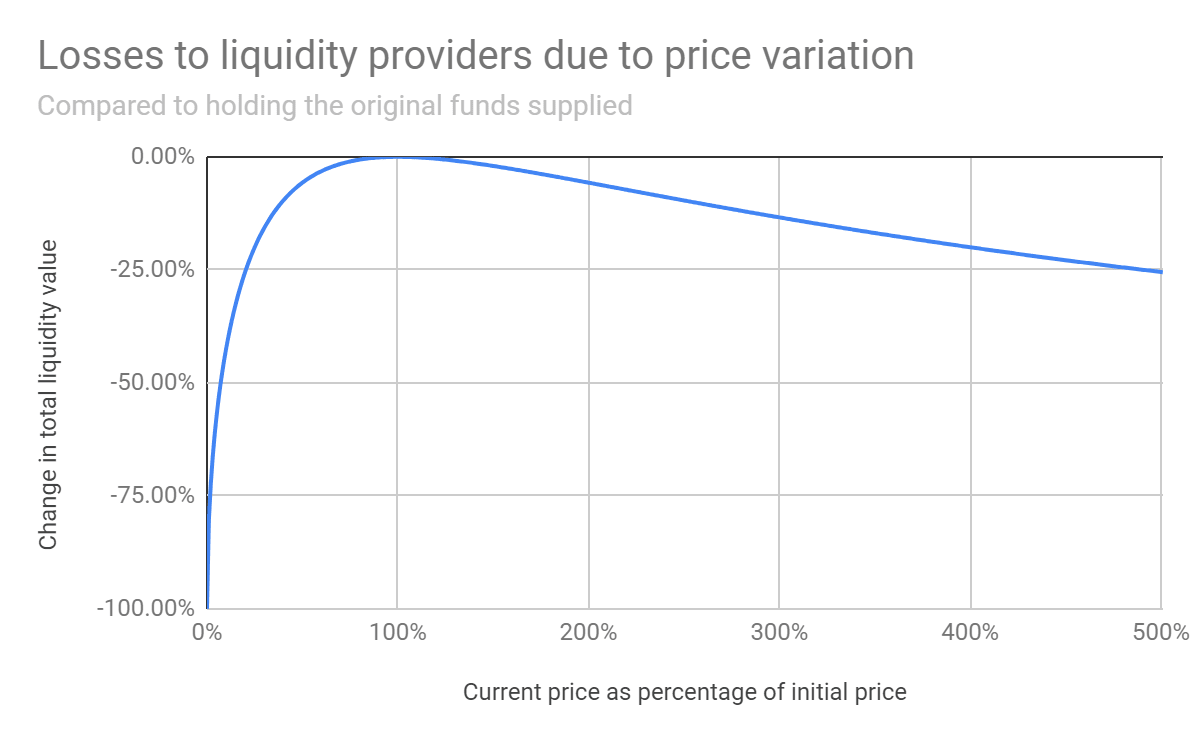

For those unfamiliar, impermanent loss is when liquidity providers lose returns on their holdings due to volatility on the trading pair. To get a brief idea of how impermanent loss can affect your pool returns, the graph below models potential losses strictly from price volatility. The graph can be read like a 500% price increase against the trading pair can result in a loss in value of 25% of your liquidity reserve.

When we consider the steps necessary towards motivating users to supply capital, it’s crucial that we explore solutions to mitigate impermanent loss seeing as it currently acts a deterrent in scenarios when LPs *should* be benefitting.

Mitigating Impermanent Loss

Stable Pools

Perhaps the most intuitive way to eliminate permanent loss is to pool liquidity across a trading pair in which the value of one asset does not appreciate or decline in value against the offer. In this sense, LP’s are able to collect fees knowing that the relationship between the two assets is more or less fixed at a 1:1 rate.

sETH - ETH

Synethetix’s version of Ether - sETH - is pegged 1:1 with Ether. While there remains a high risk profile due to the fact that sETH is *currently* largely backed by SNX (rather than ETH) the concept of supplying liquidity to a pool which has an even peg means that LPs should not have to worry about one asset’s price increasing drastically relative to the other (the two assets move in parallel).

With this, regardless of whether the price of ETH increases or decreases, LPs can know that their rewards will not suffer from impermanent loss.

Paired with underlying liquidity incentives (described below), it’s no surprise the sETH is currently the largest pool on Uniswap.

wETH - ETH

Similar to the concept described above, wrappers provide a great mechanism to pool liquidity while eliminating impermanent loss. Perhaps the easiest example of this is wrapped Ether, which *should* always trade 1:1 with Ether.

Moving forward, we can envision an ecosystem in which assets beyond ETH are being wrapped and pooled on DEXs, effectively allowing the same principle to apply on something like a wBTC/BTC liquidity pool using tools like RenVM.

Curve

Curve is an exchange liquidity pool designed for extremely efficient stablecoin trading with low risk and supplemental fee income for liquidity providers - all without an opportunity cost.

Curve allows users (and smart contracts like 1inch) to trade between DAI and USDC with a bespoke low slippage, low fee algorithm designed specifically for stablecoins. Behind the scenes, the liquidity pool is supplied to the Compound protocol, where it generates income for liquidity providers.

Curve uses cTokens, assets inside the Compound protocol, as the liquidity pool - this ensures that assets are always being put to work.

Seeing as Curve pools liquidity from stablecoins, we can effectively *know* that the relationship will always sit at 1:1.

Furthermore, Curve is able to offer some of the highest lending rates on the market (currently 11.56% at the time of writing) specifically by aggregating returns across the lending ecosystem to find the most profitable rates. To date, Curve has aggregated roughly $600k of stablecoin volume in it’s short tenure as a stealth Alpha.DAI:

2993.9

iEarn

Speaking of stablecoin liquidity aggregators, the past few weeks have seen the rise of iEarn, a solution leveraging a version of Curve’s yTokens to collect trading fees on top of liquidity provided to the protocol.

In short, iearn is a yield aggregator for lending platforms that rebalances for highest yield during contract interaction. It currently supports $DAI, $USDC, $USDT and $TUSD while aggregating lending rates across Compound, Fulcrum (currently disabled), dYdX, Aave and DDEX.

The purpose of y.curve.fi is to further increase rewards on iearn.finance tokens. After you deposit $DAI into iearn.finance you receive $yDAI. You can provide $yDAI as liquidity to y.curve.fi, meaning LPs earn trade fees (0.04% per trade) on top of yield rewards.

Leveraged Liquidity Positions

DeFiZap LLPs

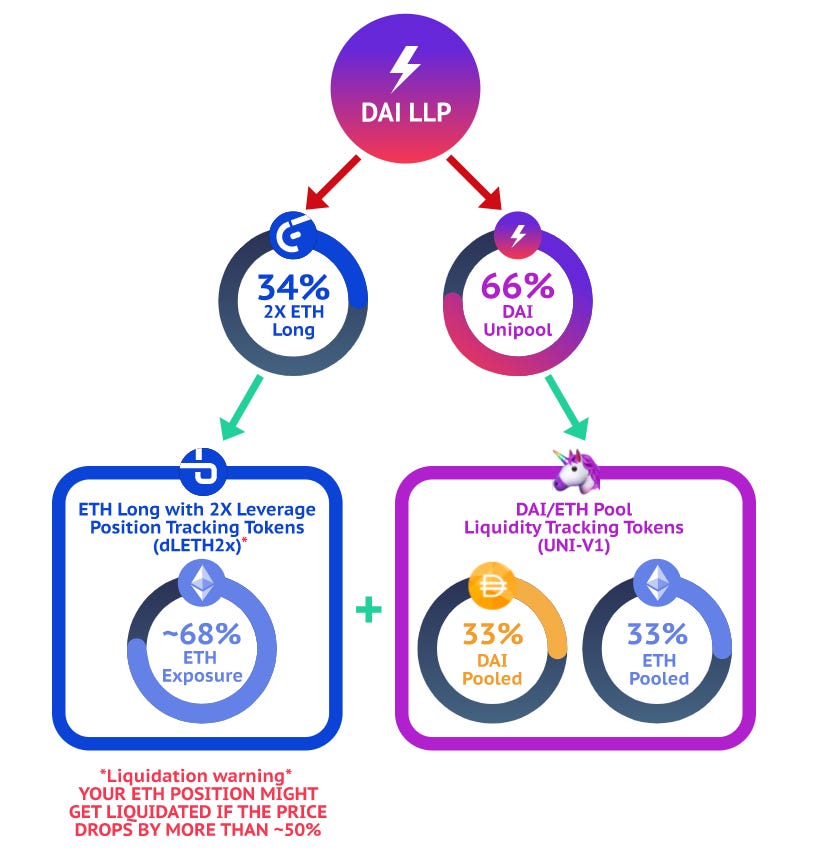

DeFiZap Leveraged Liquidity Pools allow you to enter a Uniswap pool while retaining 100% long exposure to an asset of your choosing.

This effectively allows LPs to:

Retain 100% asset exposure

Generate 66% of the fees from the underlying Uniswap pool

Eliminate impermanent loss when the price of the long asset increases.

For those unfamiliar with DeFiZap, LLPs are entered using Ether, while the protocol seamlessly converts to the underlying assets in one simple click.

Tying this back into the notion of mitigating impermanent loss, this is a different case in which the underlying liquidity pool is not 1:1. However, by using a leveraged long position on Fulcrum, LPs can know that as the price of an asset increases, the impermanent losses are offset by the profits made off the leveraged trade.

Here’s a good resource to further understand DeFiZap LLPs.

Now that we’ve covered a number of different ways to eliminate or mitigate impermanent loss on an underlying capital pool, let’s shift gears to how projects are using liquidity incentives to further motivate users to supply capital on DEXs like Uniswap.

Liquidity Incentives

With Synthetix’s success directing a portion of the protocol’s native inflation towards Uniswap LPs, the idea of liquidity incentives should slowly become common practice for many DeFi protocols.

In short - liquidity incentives can help mitigate impermanent loss as the returns earned from the subsidy reduces the loss from volatility. Importantly, they create an incentive for anyone to contribute liquidity for that respective ecosystem.

With this, there’s two potential designs for incentivizing Uniswap pools: native inflation or directing protocol revenues.

Native Inflation

Tokenized protocols can leverage native inflation to incentivize liquidity at the cost of diluting the supply. This is seen with Synthetix and their recent surge in liquidity. After Synthetix implemented its Uniswap incentive program, the sETH - ETH pool experienced explosive growth, quickly establishing itself as the most liquid pool to date.

Graph via Uniswap to $1B?

One of the reasons Synthetix is able to make this sacrifice with native inflation is largely due to the importance of sETH for the long-term success of the protocol. Ultimately if a tokenized protocol already has inflation implemented into its economic model, it may be wise to direct a portion of that inflation to LPs.

Better yet, taking advantage of sETH liquidity incentives is easy - simply stake Uniswap LP tokens via Mintr and automatically earn SNX on a weekly basis. Here’s a guide on how to get started.

Protocol Revenues

The other potential design is directing a portion of protocol revenues. This could be a good design choice for a project like Maker, where the protocol is generating millions in revenue. With Dai’s circulating supply nearing 150M, Maker is estimated to generate $6.43M in annualized earnings

Bankless “Are DeFi Tokens Worth Buying”

Today, there’s one existing platform directing revenues to liquidity providers - RealT. The tokenized real estate investment platform allows global users to invest in fractional shares of real estate properties in the Detroit area.

Earlier this year, RealT announced that they would be depositing 15% of the supply from one of their properties into a Uniswap incentive pool. This is possible as RealT retains a percentage of all properties tokenized on the platform. The tokens generate cash flows from rental incomes, and the company has elected to direct those rental incomes into this liquidity program. Since then, the Patton property quickly became the most liquid property out of any of their other pools.

Key Takeaways

Impermanent loss is by far one of the biggest detriments to the success of DEXs like Uniswap. Times of strong volatility have shown to negatively affect liquidity returns - as seen with the small bull run the past few months where liquidity pools like REP, SNX, and USDC experienced significant losses in the past 30 days

30D Annualized Return for Uniswap Pools via Blocklytics.

The importance of liquidity incentives should not be underestimated. In finance, liquidity is everything. This holds true as well with its decentralized counterpart. DeFi has the ability to leverage this new paradigm in global finance to direct protocol or network cash flows as an open incentive for anyone to provide liquidity. Not only does this boost the willingness to participate but it also plays an added role in mitigating the effects of impermanent loss.

As we’re beginning to understand Uniswap and its potential, it will be interesting to see ways in which we can attempt to mitigate impermanent loss in a seamless and intuitive fashion.

DeFi Zap’s LLPs are the closest thing we have today but they only eliminate upwards volatility while doubling-down on negative (or vice versa). If done correctly and combined with native incentives, Uniswap as a permissionless liquidity protocol will propel itself towards becoming an unstoppable force for the proliferation of open finance.

In the meantime, be sure to stay up on the latest trends within the web3 ecosystem by following us on Twitter.